Halifax Index 2021

Rural

You are viewing the 2021 Halifax Index.

To view the current edition, click here.

Resilience in Rural Halifax

Just like the rest of Halifax, rural Halifax was hit hard by COVID-19. In 2020, housing prices in rural Halifax grew by 20%, and 43% of rural residents cited difficulty regarding the availability of affordable housing. However, when rating the overall quality of life in Halifax, rural residents gave a higher average score than their urban counterparts.

Residents’ ratings of public transit proximity, schedules, and frequency improved in 2021. Though transit affordability fell slightly, across benchmark cities, Halifax offered one of the lowest transit fares. Urban residents rated aspects of transit more highly than rural residents, but the urban-rural gap on this issue is narrowing.

COVID-19 Recovery

In terms of reported difficulties related to the pandemic, rural residents fared better, on average, than urban residents on all issues covered in the City Matters Survey. Among rural residents, 79% reported feeling confident about Halifax’s recovery coming out of the pandemic, and 77% reported feeling confident about their own household situation. Both these confidence levels are higher than those reported by urban respondents.

Jump to a section

Halifax Index 2021

COVID-19 & Rural Halifax

Just as different industries felt the pandemic’s effects in varying magnitude, Halifax’s rural and urban residents also faced varying difficulties during the pandemic. Results from MQO Research’s City Matters Survey provide insight into these differences and spotlight challenges and expectations related to Halifax’s economic recovery. It is important to keep in mind, though, that these results were collected before the city experienced its third wave of COVID-19 cases.

Among rural residents, 70% expect Halifax to return to normal sometime in 2022 or beyond compared to 49% of urban residents. Fewer than 5% of both rural and urban residents expect a return to normalcy very soon. However, a majority of both rural (79%) and urban (71%) residents are confident in Halifax’s economy coming out of the pandemic. This optimism could be due to the tremendous growth the city experienced pre-pandemic. Additionally, 77% of rural residents were confident regarding their own household’s economic situation coming out of the pandemic, 5 percentage points higher than urban respondents.

When looking at difficulties faced by residents due to COVID-19, rural residents rated a lower mean level of difficulty across all survey areas than their urban counterparts. The issue that created the highest concerns for both rural and urban residents was their mental health, and the lowest reported difficulty was with connectivity (broadband and Wi-Fi).

Most residents in rural areas are hesitant to go out to a bar or a movie, and roughly half of rural residents would only be comfortable with such activities once everyone has been vaccinated or herd immunity has been achieved. On the other hand, a higher share of urban residents are already comfortable with all seven activities surveyed.

Businesses in the construction industry hold the largest share of locations in rural Halifax according to Statistics Canada’s Canadian Business Counts. More than 25% of businesses in both Western Rural and Inner Rural/Commuter Halifax are in construction. Urban Halifax is dominated by professional, scientific, and technical services, and retail and wholesale trade.

-

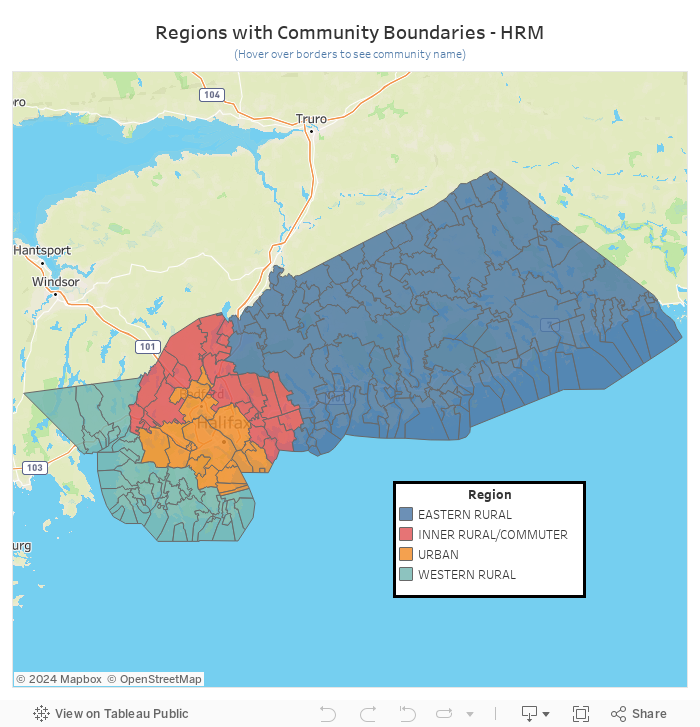

Rural Regions

- Halifax has the largest rural population across all counties in Nova Scotia.

- Halifax has the largest proportion of rural citizens among census metropolitan areas in Canada.

- Aggregations of census tracts are used to define Urban Halifax and three rural areas: Inner Rural/Commuter, Eastern Rural, and Western Rural.

-

DIFFICULTIES FACED DUE TO COVID-19

Mean Scores (1 to 10) and Share of Residents, Halifax, 2021

Rural

Urban

Difficulties with Child Care Situation

3.0

3.9

Difficulties with Income

3.3

4.1

Difficulties with Mental Health 4.25.0Difficulties with Employment 3.44.1Challenges in ability to get around (transit, taxi, etc.) 2.73.3Difficulties with Connectivity (broadband, Wi-Fi) 2.52.8Difficulties with Physical Health 3.84.1% Comfortable to ride the bus now 18%33%

% Comfortable to go to a movie, game, or concert now 12%22%% Comfortable to ride a taxi now 27%37%% Comfortable to go to a bar now 19%26%% Comfortable to board a plane now 7%12%% Comfortable to go to a restaurant now 49%49%% Comfortable to go to a store now 78%77%Source: MQO Research, City Matters Survey (2021)

COVID-19 Difficulties

- Mean scores for questions regarding difficulties faced due to COVID-19 were below 5 for both rural and urban residents. Rural respondents had lower mean scores than urban residents for all questions, and the largest gap between the two was for child care.

- The highest difficulty rating for both urban (5.0) and rural (4.2) residents was for mental health. The lowest difficulty rating was for connectivity issues for both urban and, perhaps surprisingly, rural respondents.

- Comfort levels for various activities were similar for rural and urban respondents – comfort in visiting a store was the highest-rated while comfort boarding an airplane was the lowest rated. The survey results were collected prior to the third wave of the pandemic, however, and views may have changed.

-

Source: Custom Tabulation Based on Statistics Canada, Canadian Business Counts, Tables 33-10-0222-01 & 33-10-0223-01

Share of Business Location Counts by Industry

- Across regions, the largest share of businesses in agriculture, forestry, fishing, and hunting was in the Eastern Rural part of Halifax.

- Businesses in construction make up a large share of industry in both the Western Rural and Inner Rural regions.

- Wholesale and retail trades dominate the Urban region followed by healthcare and social assistance.

Halifax Index 2021

Rural Living

Questions in the City Matters Survey about affordability, concerns, and employment provide insight into rural and urban residents’ views about their general economic well-being.

General affordability is a growing concern in all parts of Halifax, but the concern is more pronounced in rural areas. In 2021, 58% of rural residents found goods and services “somewhat difficult to afford,” or “very difficult to afford,” up 18 percentage points from 2020.

When asked about the most important issues facing the city in 2021, “affordability/cost of living” ranked the highest for both rural and urban residents. Similarly, affordable housing was the top issue for rural and urban residents in 2020.

“Lowering taxes” was the second major issue for rural residents, increasing by 19 percentage points (the largest increase across all options). Concerns regarding COVID-19 were an important issue in 2021 with 16% of rural and 12% of urban residents citing it as the most pressing issue.

Employment has a major impact on most households’ abilities to afford goods and services. Halifax was leading all Canadian cities in employment growth in early 2021, and the overall share of employed residents who expected their employment to be stable (79% for rural and 86% for urban residents) increased over 2020. However, 18% of rural residents and 12% of urban residents still do not expect their employment to be stable over the next year.

-

OPINIONS ON AFFORDABILITY OF GOODS AND SERVICES

Share of Respondents, Rural and Urban Halifax, 2020 and 2021

2020

2021

Rural

Urban

Rural

Urban

Very easy to afford

3%

3%

3%

6%

Somewhat easy to afford

57%

59%

38%

42%

Somewhat difficult to afford

33%

30%

43%

39%

Very difficult to afford

7%

6%

14%

12%

Source: MQO Research, City Matters Survey (Various)

Affordability

- Compared to 2020, a larger share of residents in Halifax stated that goods and services have become more difficult to afford. In fact, the share of residents who find goods and services “very difficult to afford” doubled in both rural and urban Halifax.

- The share of rural residents who stated goods and services were “somewhat difficult to afford” has increased by a substantial 10 percentage points in 2021.

- The total share of rural respondents who cited difficulty with affordability has jumped from 40% in 2020 to 58% in 2021; for urban respondents, the increase went from 37% to 51%.

-

MOST IMPORTANT ISSUES FACING THE CITY

Share of Respondents, Rural and Urban Halifax, 2021

Rural

Urban

Affordability/cost of living

31%

47%

Lowering taxes

23%

11%

Handling the COVID pandemic

16%

12%

Ensuring growth is sustainable

9%

9%

Economic growth

6%

9%

Ensuring growth is inclusive

4%

2%

Improving access to labour/more workers

2%

4%

Less red tape/bureaucracy

4%

1%

Other

3%

2%

Don't know

1%

2%

Prefer not to say

0%

1%

Source: MQO Research, City Matters Survey (2021)

Important Issues

- When asked to name the most pressing issues in Halifax, both rural (31%) and urban (47%) residents agreed that “affordability/cost of living” is the most important. In the 2020 survey, this question asked specifically about “affordable housing.” In that survey, 19% of rural residents and 27% of urban respondents, said this was a major issue. The change from 2020 to 2021 indicates a large increase in concern.

- The share of residents who think it is important to lower taxes increased by 19 percentage points for rural and 8 for urban residents.

- Only 16% of rural residents consider handling the COVID pandemic as a top issue for the city in 2021.

-

EXPECTATIONS OF EMPLOYMENT STABILITY OVER THE NEXT YEAR

Share of Respondents, Rural and Urban Halifax, 2020 and 2021

2020

2021

Rural

Urban

Rural

Urban

Very stable

41%

46%

39%

48%

Somewhat stable

38%

35%

41%

38%

Not very stable

10%

8%

13%

9%

Not at all stable

7%

5%

5%

4%

Don’t know

4%

6%

3%

1%

Source: MQO Research, City Matters Survey (Various)

Employment Stability

- Expectations regarding job stability have remained reasonably unchanged for both rural and urban residents in 2021 over 2020.

- Most rural residents (79%) expect their employment to be either “very stable” or “somewhat stable,” roughly the same as last year. However, the “very stable” share of rural residents fell by 2 percentage points. Among urban residents, 86% expected stable employment, a 5 percentage point increase.

- The share of those who think their employment is “not at all stable” fell by 2 percentage points among rural residents. However, the “not very stable” share increased by 3 percentage points. Similar changes were recorded for urban residents.

- The share of those unsure about their employment stability has also decreased since 2020.

Halifax Index 2021

Rural Housing

Halifax experienced record housing price increases in 2020, and consequently, residents’ rating of housing affordability fell. According to the 2021 City Matters Survey, 11% of rural residents and 18% of urban residents rated the availability of housing affordability “very poor.” On the other end of the scale, only 1% of rural and 4% of urban residents rated the availability of housing affordability as “excellent.”

In 2020, housing-market indicators in rural areas of Halifax pointed to supply being unable to match demand. Faster price growth in rural areas, coupled with high sales-to-listings ratios and low months of housing inventory, suggest that higher demand is spreading toward rural areas as a result of market conditions in urban areas.

Increases in home prices were not just concentrated in urban Halifax. After modest single-digit rates in 2019, price growth in rural1and urban2 areas of Halifax was at least 15% in 2020.

The increases in prices were higher in rural (20%) than in urban (15%) areas though the average price is still higher in urban Halifax by about $41,000.

Another important indicator in assessing housing markets is the sales-to-new-listings ratio3. In 2020, all rural and urban areas of Halifax had a ratio of 80 or higher, indicating a seller’s market. Rural areas showed higher growth than urban Halifax, with the Western Rural area jumping the most from 2019 (up 24.7%).

Similarly, months of housing inventory4 indicates how long current inventory would last if no houses were added moving forward. In 2020, the highest level of this inventory was seen in the Eastern Rural area at 3.9, a significant drop when compared to the 2019 figure of 8.9. The level dropped from 2.9 to 1.7 in urban Halifax.

-

RESIDENTS’ RATING OF HOUSING AFFORDABILITY

Share of Respondents, Rural and Urban Rural Halifax, 2019 to 2021

Scale

2019

2020

2021

Rural

Urban

Rural

Urban

Rural

Urban

1 - Very Poor

11%

5%

9%

11%

11%

18%

2

3%

4%

5%

6%

9%

11%

3

8%

10%

8%

8%

10%

16%

4

3%

10%

14%

12%

11%

11%

5

15%

16%

10%

13%

19%

8%

6

16%

15%

10%

15%

8%

11%

7

12%

14%

16%

13%

10%

8%

8

12%

8%

10%

6%

9%

5%

9

5%

6%

5%

5%

2%

2%

10 - Excellent

3%

2%

3%

2%

1%

4%

Not applicable

2%

2%

2%

2%

4%

2%

Prefer not to say

0%

0%

0%

1%

0%

0%

Don't know

10%

7%

8%

6%

5%

2%

Source: MQO Research, City Matters Survey (Various)

Affordability

- The share of urban residents rating Halifax’s housing affordability as “very poor” has increased 13 percentage points in two years. Comparatively, for rural residents this share (11%) has not changed since 2019.

- Over the past three years, no more than 4% of rural or urban residents have rated Halifax as “excellent” with respect to housing affordability.

- More broadly, the share of rural and urban residents with a rating on the lower side (1-5) has increased 21 and 20 percentage points, respectively, since 2019. Correspondingly, there have been declines of 18 and 16 percentage points, respectively, on the higher side (6-10) of the scale over the same period.

-

AVERAGE HOME SALE PRICE

Current Dollars, Halifax, 2018 to 2020

Year

Halifax Average

Rural Areas

Urban Area

Rural Total

Inner Rural

Eastern Rural

Western Rural

2018

$302,274

$275,580

$276,129

$272,219

$277,089

$315,882

2019

$321,910

$286,414

$289,137

$296,159

$276,288

$333,004

2020

$369,435

$342,988

$340,984

$344,535

$344,627

$384,178

Includes both new and resale homes.

Source: Nova Scotia Association of REALTORS, Halifax-Dartmouth Residential Market Activity (Various)Home Prices

- Home prices have been rising across all regions of Halifax in the past few years, with total rural price growth (+20%) surpassing growth in urban areas (15%) during 2020.

- Price growth in Western Rural Halifax (+25%) was the highest across the municipality.

- Although growth has been faster in rural areas, the average price remains 12% higher in urban Halifax.

-

SALES-TO-NEW-LISTINGS RATIO

Sum of Sales Divided by Sum of New Listings, Halifax, 2018 to 2019

Year

Halifax Average

Rural Areas

Urban Area

Rural Total

Inner Rural

Eastern Rural

Western Rural

2018

65.0

62.1

63.9

54.4

64.9

70.8

2019

78.6

72.4

79.3

55.9

74.3

83.2

2020

88.8

88.1

90.5

81.5

89.3

89.1

Source: Nova Scotia Association of REALTORS, Halifax-Dartmouth Residential Market Activity (Various)

Sales to New Listings

- In 2020, the sales-to-new-listings ratios across Halifax were all over 80. A higher ratio (>55) implies a seller’s market, more buyers chasing a smaller number of homes. A lower ratio (<45) implies a buyer’s market, fewer buyers chasing a larger number of homes.

- All areas experienced an increase in the ratio; however, the largest jump was seen in the Eastern Rural area of Halifax where the market was somewhat balanced (ratio = 50) just a year ago.

- As home prices increased in urban Halifax, demand grew in the more rural areas, and supply has been limited throughout 2020. This has consequently led to an increase of at least 10 points in the ratio throughout rural Halifax.

-

MONTHS OF HOUSING INVENTORY

Inventory Divided by Average Units Sold per Month, Halifax, 2018 to 2020

Year

Halifax Average

Rural Areas

Urban Area

Rural Total

Inner Rural

Eastern Rural

Western Rural

2018

5.9

7.3

6.2

9.5

7.2

4.7

2019

3.9

5.9

4.3

8.9

6.0

2.9

2020

2.2

2.9

2.4

3.9

2.8

1.7

Source: Nova Scotia Association of REALTORS, Halifax-Dartmouth Residential Market Activity (Various)

Housing Inventory

- Months of housing inventory5, 6fell across all regions of Halifax in 2020, but the decline was sharper in rural Halifax.

- With supply not being able to keep up with demand, the number of months a listing lasted on the market decreased. As mentioned earlier, with increases in urban home prices, consumers shifted their demand towards rural Halifax.

Halifax Index 2021

Rural Transportation

Halifax compares well to benchmark cities in terms of transit fares, and residents’ ratings of the quality of public transit are improving yearly, particularly among residents of rural Halifax.

Although urban residents still rate aspects of transit quality higher than rural residents on a scale of 1 (very poor) to 10 (excellent), survey responses show a narrowing gap between rural and urban respondents. The rural-urban gaps in mean scores for all three aspects of transit quality (proximity, convenience, and frequency) dropped by approximately 1 full point from 2020 to 2021.

When comparing transit affordability ratings, rural residents were more inclined to state affordability was “very poor” and less inclined to call it “excellent.” Looking more broadly at those who gave a score of 1 to 5 versus those who gave a score of 6 to 10, rural and urban shares were very similar. Mean scores on the affordability question were similar as well, at 6.6 for rural respondents and 6.8 for urban respondents.

-

CITIZEN RATINGS OF TRANSIT QUALITY

Mean Scores (1 to 10), Rural and Urban Halifax, 2020 and 2021

2020 Mean Score

2021 Mean Score

Rural

Urban

Rural

Urban

Buses stop close to where you live and work

4.6

7.8

6.2

8.0

Buses run on schedules that are convenient for you

4.7

6.4

5.4

6.3

Buses arrive frequently and wait times are short

5.3

6.1

6.2

6.3

Source: MQO Research, City Matters Survey (Various)

Transit Quality

- Overall, rural residents again have lower mean ratings for transit quality compared to urban residents although the gaps have narrowed from 2020 to 2021.

- The biggest urban-rural gap, at 1.8 points, was around whether buses stop close to where respondents live and work.

- Rural residents’ mean ratings improved on all three aspects of transit quality from 2020 to 2021. Mean ratings from urban residents rose by 0.2 points on two items and fell by 0.1 point on another.

-

Answers of "Don't know" and "No Answer" were excluded.

Source: MQO Research, City Matters Survey (2021)Citizen Ratings of Public Transit Affordability

- Although transit fares in Halifax are either the lowest or second lowest across benchmark cities, 5% of rural residents and 2% of urban residents rated transit affordability as “extremely poor” (1 out of 10).

- There were 14% of urban residents who viewed transit affordability as “excellent” (10 out of 10) compared to only 8% of rural residents.

- Rural and urban residents were almost identical in terms of the total share who gave ratings of 5 or lower and the total share who gave ratings of 6 or higher on the issue of affordability.